Selling US real estate as an expat: FIRPTA, capital gains & tax planning

US citizens abroad are not subject to FIRPTA, which is the most common misconception when selling US property from overseas. Here's what actually applies: capital gains, the 121 exclusion after years abroad, state source-income tax, and when FIRPTA does come into play.

Many American expats assume that selling a US property from abroad means managing FIRPTA withholding. For most of the SavvyNomad audience, that assumption is wrong, and understanding why changes the entire picture.

FIRPTA applies to foreign persons selling US property: nonresident aliens and foreign entities. It does not apply to US citizens or Green Card holders living abroad, because they are not "foreign persons" under US tax law. They are still US tax residents, paying standard federal capital gains tax and filing a regular Form 1040, not the nonresident 1040-NR.

What US citizens abroad do face is a different set of questions: whether the 121 primary residence exclusion still applies after years living overseas, how to calculate the gain correctly (especially if the property was ever rented), what state income tax the sale triggers in the property's source state, and when FIRPTA does apply: for foreign national co-owners, relinquished Green Card holders, and certain covered expatriates.

This guide starts with the situation that applies to most readers, then covers FIRPTA for those who need it.

US citizens and Green Card holders living abroad are not subject to FIRPTA; that's the most common misconception in this area. They pay standard federal capital gains tax and report on Form 1040. The 121 primary residence exclusion ($250,000 single / $500,000 married filing jointly) may still be available, but the 2-of-5-year use test is more challenging for expats who haven't lived in the property for several years. State income tax on gains from in-state property applies regardless of where the seller now lives. For foreign nationals, relinquished Green Card holders, and covered expatriates, FIRPTA withholding of 15% on the gross sale price applies at closing and is collected by the buyer, with any excess recovered via Form 1040-NR. Plan before the sale closes, not after.

US citizen abroad or foreign national? The answer changes your entire tax picture

The single most important question for any expat selling US property is tax status, not citizenship, not visa type, but US tax residency.

US citizens and Green Card holders are US tax residents regardless of where they physically live. They are not "foreign persons" under FIRPTA. When they sell US property, they pay standard federal capital gains tax, report the sale on Form 1040, and may claim the 121 exclusion if they qualify. FIRPTA withholding does not apply to their sale.

Nonresident aliens and former US persons, including those who have formally relinquished a Green Card after long-term residency, are foreign persons under US tax law. FIRPTA withholding applies to their sale. They report the gain on Form 1040-NR and claim any over-withheld amount as a refund.

One scenario that regularly creates confusion: a mixed-status couple where one spouse is a US citizen and the other is a foreign national, and both are co-owners of the property. The US citizen co-owner's share is generally not subject to FIRPTA; the foreign national co-owner's share may be. The withholding calculation becomes fact-specific; get professional advice before closing.

One more point that belongs here: IRC 121(e) explicitly denies the primary residence exclusion to covered expatriates - individuals subject to the exit tax rules under 877(a)(1). If you are in the process of renouncing citizenship and are a covered expatriate, the 121 exclusion is not available to you. That intersection is covered in our US exit tax guide.

For US citizens and Green Card holders abroad: your capital gains picture

Calculating the gain

The taxable gain on a property sale is net proceeds minus adjusted cost basis.

Adjusted cost basis includes: the original purchase price, closing costs paid at acquisition (title insurance, legal fees, transfer taxes), and capital improvements made during ownership (a new roof, an extension, a kitchen remodel). It does not include routine maintenance or repairs.

Net proceeds are the sale price minus selling costs: agent commissions, closing costs, legal fees, and any repairs required as a condition of the sale.

Depreciation recapture is the most commonly missed item. If the property was rented at any point and depreciation was claimed, or should have been claimed, that amount reduces your cost basis and must be recaptured at ordinary income tax rates of up to 25% when you sell. Depreciation recapture cannot be excluded under 121; it applies to any depreciation taken after May 6, 1997, regardless of whether the rest of the gain qualifies for the exclusion. "I never actually claimed depreciation" is not a defense; the IRS recaptures the "allowed or allowable" amount.

Federal capital gains rates

Long-term gains (property held over one year) are taxed at 0%, 15%, or 20% depending on taxable income. For 2026, the 15% rate applies to single filers up to $ 545,500 and to married filers filing jointly up to $613,700; gains above those thresholds are taxed at 20%. The 3.8% Net Investment Income Tax applies to gains above $200,000 (single) or $250,000 (married filing jointly) — these thresholds are not adjusted for inflation.

Short-term gains (held one year or less) are taxed as ordinary income at rates up to 37%.

Report the sale on Form 1040, Schedule D, and Form 8949. If depreciation recapture applies, also file Form 4797.

The 121 primary residence exclusion: do you still qualify after years abroad?

This is the highest-value section for most expat property sellers. The §121 exclusion can eliminate federal tax on the entire gain, but years of living abroad erode eligibility in ways many sellers don't anticipate until it's too late.

What the exclusion covers

The §121 exclusion allows up to $250,000 of capital gain to be excluded for single filers, and up to $500,000 for married couples filing jointly. To qualify, you must have owned the property for at least 2 of the last 5 years (ownership test) and used it as your primary residence for at least 2 of the last 5 years (use test). Both tests apply. The 5-year lookback runs from the sale date, not from when you left.

The 24 months of use do not need to be continuous — you can aggregate qualifying periods within the 5-year window. Short temporary absences (a vacation, a short work trip) generally count as periods of use. A multi-year relocation abroad does not.

How years abroad affect eligibility

Time spent living abroad does not count toward the "use" requirement. The IRS regulations make this explicit: a one-year sabbatical abroad, for example, is not a short temporary absence and cannot be included in the use period.

The practical impact: an expat who moved abroad 3 years ago and hasn't returned to live in the property has used it for roughly 2 of the last 5 years — right at the threshold. One more year abroad without a sale, and eligibility disappears entirely. An expat 4 or more years out is likely no longer eligible for the full exclusion.

The ownership test is easier to preserve — you can own the property without using it. It is possible to fail the use test while still passing the ownership test, which creates partial exclusion eligibility.

The partial exclusion, what it covers and how it's calculated

If the full 2-year use test isn't met, a reduced exclusion may still apply if the primary reason for the sale was a change in employment, a health condition, or other unforeseen circumstances as defined by IRS regulations. Moving abroad for work qualifies as a "change in place of employment," but whether a specific situation satisfies the IRS definition is fact-specific, and professional confirmation matters here.

The partial exclusion is calculated proportionally: the fraction of the 24-month requirement that was met, multiplied by the full $250,000 or $500,000 limit. An expat who lived in the property for 12 months out of the required 24, selling due to a work relocation abroad, may exclude 50% of the standard amount, up to $125,000 for a single filer.

The suspension rule for foreign service and military

A narrower but useful provision: members of the military and certain government foreign service and intelligence personnel on extended duty may suspend the 5-year period for up to 10 years, effectively extending the window during which the use test can be satisfied. This doesn't apply to most SavvyNomad readers but is worth knowing.

Tax breaks for American nomads and expats

For foreign nationals selling US property, how FIRPTA withholding works

FIRPTA (Foreign Investment in Real Property Tax Act, IRC 897 and 1445) ensures the IRS collects tax on gains from foreign sellers before they leave US jurisdiction. The buyer, not the seller, is the withholding agent and is personally liable if the correct amount is not withheld and remitted on time.

FIRPTA withholding is not the final tax. It's computed on the gross amount realised; the seller's actual tax is calculated on net gain and reported on Form 1040-NR. If withholding exceeds actual tax liability, which is common, particularly on high-basis properties, the seller recovers the excess by filing Form 1040-NR and attaching the IRS-stamped Form 8288-A.

Withholding rates

The standard rate is 15% of the gross amount realized: the full sale price, including liabilities the buyer assumes, not just the gain. Reduced rates apply based on sale price and the buyer's intended use: 0% for sales under $300,000 where the buyer intends to use the property as a primary residence; 10% for sales between $300,000 and $1,000,000 for buyer's primary residence; 15% for all sales over $1,000,000 regardless of use.

The residence exception requires a buyer affidavit confirming intent to occupy the property for at least 50% of the days it is used over the next two years. If the buyer won't sign one, the full 15% applies.

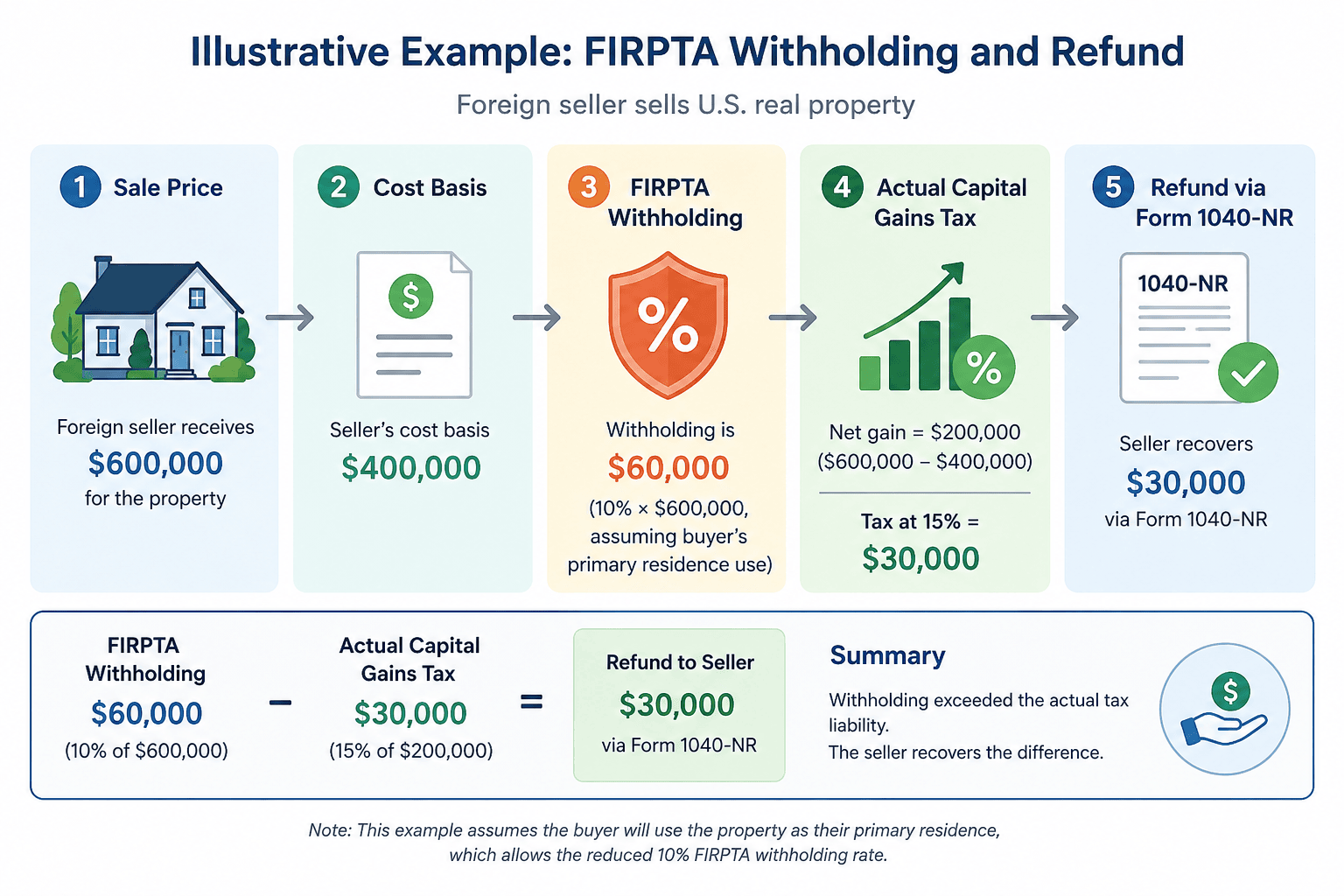

Illustrative example: a foreign seller receives $600,000 for a property with a $400,000 cost basis. FIRPTA withholding is $60,000 (10% × $600,000, assuming buyer's primary residence use). Actual capital gains tax on the $200,000 net gain at 15% = $30,000. The seller recovers $30,000 via Form 1040-NR.

Key forms and timeline

Form 8288 (buyer's withholding return) must be filed within 20 days of the transfer date. Form 8288-A is the seller's withholding statement, the IRS stamps Copy B and returns it to the seller to attach to Form 1040-NR as the withholding credit.

Form 8288-B is an application to reduce withholding, filed by the seller before closing. If the seller doesn't yet have a US Individual Taxpayer Identification Number (ITIN), applying for one takes 7-11 weeks, begin well before closing.

FIRPTA and 1031 exchanges

FIRPTA withholding applies even when the sale is part of a §1031 like-kind exchange. Withheld funds can't be used to purchase the replacement property, potentially breaking the exchange.

The solution is to apply for a Form 8288-B withholding certificate before the exchange closes, or to deposit equivalent funds with the qualified intermediary. This requires tight coordination between a FIRPTA specialist and the exchange intermediary, do not assume FIRPTA is automatically deferred simply because the transaction is structured as a 1031 exchange.

State capital gains tax

A US citizen living in Lisbon who sells a rental property in California owes California income tax on the gain. Not because they're a California resident. Because the property is in California, and California taxes gains on in-state property regardless of where the seller currently lives.

Several states like California, New York, Virginia, South Carolina, and others apply source income rules to real property gains. A former resident who has cleanly changed domicile to Florida still owes California tax on the sale of California property. State withholding may also apply at closing, separate from and in addition to FIRPTA at the federal level.

The practical implication for expats: if retaining a property in a former high-tax state was part of the reason you haven't fully exited that state's tax base, selling the property may also close the final remaining tie, but it generates a taxable event in that state regardless of domicile.

- Do I owe state income tax if I live abroad?

- California exit tax explained

- What to expect in a residency audit

Tax planning before you sell

The decisions that affect your tax bill most are made before you accept an offer, not after.

- Watch the 121 clock. If your 2-of-5-year use window is approaching expiration, selling before it does preserves access to the full exclusion, which can be worth $250,000 to $500,000 in federal tax savings on a high-value property. Run the numbers before accepting that the sale can wait another year.

- Document your cost basis before closing. Gather all purchase records, original closing statements, and receipts for capital improvements. Missing basis documentation is one of the most common ways sellers overpay on property gains, and reconstructing records after the sale is far harder than before it.

- Account for depreciation recapture. If the property was rented for any period, work out the recapture exposure with a CPA before accepting an offer. The one-time income spike from recapture can push the seller into a higher bracket and affect other tax calculations for the year.

- Check treaty implications. If you live in a country with a US tax treaty, the treaty may reduce or eliminate tax on the gain in your country of residence, or affect how the US gain interacts with a foreign tax credit. Treaty analysis is fact-specific.

- Get professional advice before closing. Property sales are among the highest-value, lowest-frequency tax events that most expats face. The cost of a cross-border CPA's review of the transaction is almost always justified.

Frequently asked questions

Do I owe FIRPTA if I'm a US citizen living abroad?

No. US citizens are not foreign persons under FIRPTA regardless of where they live. You pay standard capital gains tax on Form 1040. Taxes on American citizens living abroad

Can I claim the 121 exclusion if I've lived abroad for four years?

Likely not the full exclusion. The 2-of-5-year use test requires actual residential use, and time abroad doesn't count. A partial exclusion may be available if the move was work-related. Consult a CPA before assuming eligibility.

My spouse is a foreign national and we co-own the property, does FIRPTA apply?

Potentially to your spouse's share of ownership. The US citizen co-owner's share is not subject to FIRPTA; the foreign national co-owner's share may be. This requires professional analysis before closing.

What is Form 8288-B and when should I file it?

An application to reduce FIRPTA withholding based on actual expected tax liability — most valuable when the 15% gross withholding would significantly exceed your real tax (high-basis properties are the typical case). File it as early as possible before closing; IRS processing takes 90 days or more.

How long does a FIRPTA refund take?

Typically 6–18 months after filing Form 1040-NR with the stamped Form 8288-A; some cases reach 18–24 months due to ITIN issues, incomplete documentation, or IRS processing backlogs.

I owe state tax on my California property sale even though I've moved to Florida?

Yes. California taxes gains on California-source property regardless of where you now live. Your domicile change to Florida affects California's ability to tax your other income — not gains on property still located in California. Do I owe state income tax if I live abroad?

The property was a rental for three years before I sold — does that change anything?

Significantly. You face depreciation recapture on the depreciation claimed (or allowable) during the rental period, taxed as ordinary income up to 25%. The §121 use test also applies to the rental period. Get professional advice before closing.

Conclusion

For US citizens and Green Card holders abroad, FIRPTA is not the issue — capital gains, §121 eligibility, depreciation recapture, and state source-income tax are. For foreign nationals and former US persons, FIRPTA is the issue, and the planning window is before the sale closes, not after.

Selling US property from abroad is one of the highest-stakes tax events most expats face. The decisions that reduce that bill — timing the sale relative to the §121 clock, documenting cost basis, understanding depreciation exposure — all need to happen before you accept an offer.

For personalized guidance on your specific situation, SavvyNomad's CPA-access service connects you with cross-border tax professionals familiar with expat property sales.