Foreign Housing Exclusion and Deduction

The Foreign Housing Exclusion (FHE) helps American expatriates reduce their taxable income by excluding certain housing costs.

This article will explain FHE, who qualifies, and how to claim it. We'll also cover related tax benefits like the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC) and discuss how moving to states with no state income tax can boost your savings.

TLDR

To qualify, you must have a tax home in a foreign country and meet either the bona fide residence or physical presence test.

The maximum exclusion for 2024 is $37,950.

Both spouses can claim the exclusion if they qualify.

Using these benefits and moving domicile to a no-tax state can maximize tax savings.

What is the Foreign Housing Exclusion?

The Foreign Housing Exclusion (FHE) allows Americans living abroad to exclude some of their housing costs from their taxable income. This can include rent, utilities, and other housing-related expenses. The main purpose of FHE is to help expatriates reduce their tax burden while living in a foreign country.

The FHE is part of the U.S. tax code and is governed by specific rules and regulations. It works alongside other tax benefits, such as the Foreign Earned Income Exclusion (FEIE). While the FEIE lets you exclude some of your foreign earnings from U.S. taxes, the FHE focuses specifically on housing costs.

The exclusion applies only to amounts paid with employer-provided funds that can be classified as taxable foreign earned income for the tax year in question.

In summary:

- FHE: Excludes housing costs from taxable income.

- FEIE: Excludes a portion of foreign-earned income from taxable income.

Both benefits can be used together to maximize tax savings.

Eligibility requirements

To qualify for the Foreign Housing Exclusion (FHE), you must meet certain criteria.

Firstly, your tax home must be in a foreign country. This means your main place of business or employment is outside the United States.

Additionally, you must pass either the bona fide residence test or the physical presence test:

- Bona fide residence test: You need to be a resident of a foreign country for an entire tax year without significant interruptions.

- Physical presence test: You need to be physically present in a foreign country for at least 330 full days during any 12-month period.

Examples of qualifying scenarios include:

- An American who has lived and worked in Germany for over a year and maintains a permanent residence there.

- An expatriate who spends at least 330 days in Japan within a 12-month period.

The FHE covers various housing expenses, such as:

- Rent: Payments for your home in a foreign country.

- Utilities: Costs for electricity, gas, water, and other services.

- Certain household expenses: Some additional costs related to maintaining your home.

Reasonable expenses cover necessary housing costs for the taxpayer, spouse, and dependents. Eligible expenses include rent and utilities, while ineligible expenses under the Foreign Housing Exclusion guidelines include luxury items, domestic help, and pay-per-use services.

However, there are limitations and caps on these exclusions. The amount you can exclude depends on the location and cost of living.

Non-qualifying expenses include:

- Luxury items: Such as furniture and home improvements.

- Domestic help: Salaries for housekeepers or gardeners.

- Pay-per-use services: Like internet and cable TV.

How to claim and calculate the Foreign Housing Exclusion

Calculating FHE

- Determine your qualified housing expenses: Include rent, utilities, and certain household expenses.

- Apply housing cost limitations: These limits vary based on your foreign location. Check the IRS guidelines for specific limits for your country.

- Calculate your exclusion: Subtract the base housing amount (usually 16% of the FEIE limit) from your total qualified housing expenses. The result is the amount you can exclude.

Knowing your total foreign earned income is crucial as it serves as the limit for excluding housing costs under the Foreign Housing Exclusion.

Example calculations

Scenario 1: You live in a country with a high cost of living and have $30,000 in qualified housing expenses. After applying the base housing amount and the country-specific limit, you might be able to exclude a significant portion of those expenses.

Scenario 2: You live in a country with a low cost of living and have $10,000 in qualified housing expenses. The exclusion might be smaller, but still beneficial.

Necessary forms and documentation

- Form 2555: Use this form to claim the FHE. You'll need to provide details about your foreign housing expenses and your eligibility (bona fide residence test or physical presence test).

- Supporting documents: Keep receipts and records of your housing expenses to support your claim.

Common mistakes and special considerations

- Incorrectly calculating expenses: Make sure to include only qualified expenses and apply the correct limits.

- Missing documentation: Keep thorough records to support your claim.

- Wrong eligibility status: Ensure you meet the bona fide residence or physical presence test requirements.

- Impact of exchange rates and currency fluctuations: Convert your expenses to U.S. dollars using the average exchange rate for the year.

- Handling mid-year moves or changes in housing costs: Adjust your calculations if you move or if your housing costs change significantly during the year.

- Maintaining eligibility: Ensure you continuously meet the residency or presence tests.

- Dealing with changing costs: Keep detailed records and adjust your calculations as needed.

- Navigating complex tax rules: Consider seeking professional tax advice if you encounter difficulties.

Additional tax benefits for expatriates

Foreign Earned Income Exclusion (FEIE)

The FEIE allows U.S. citizens living and working abroad to exclude a certain amount of their foreign earnings from U.S. taxation.

Eligibility requirements and how it complements FHE:

To qualify, you must have a tax home in a foreign country and meet either the bona fide residence test or the physical presence test. This exclusion works alongside the FHE by allowing you to exclude both foreign-earned income and housing expenses.

Both exclusions apply to taxable foreign earned income, which is crucial for qualifying for the exclusions as it includes amounts paid with employer-provided funds that can be classified as taxable foreign earned income for the tax year in question.

Example scenarios showing the combined use of FEIE and FHE:

- Scenario 1: An expatriate in Germany earns $120,000 and has $30,000 in housing expenses. They can use the FEIE to exclude a portion of their income and the FHE to exclude housing costs.

- Scenario 2: An expatriate in Japan earns $90,000 and has $20,000 in housing expenses. They can maximize their tax savings by using both FEIE and FHE.

Foreign Tax Credit (FTC)

The FTC allows U.S. taxpayers to claim a credit for taxes paid to foreign countries, reducing the double taxation burden.

Eligibility requirements and how they differs from FHE and FEIE

You must pay or accrue taxes to a foreign country on income that is also subject to U.S. tax. Unlike FHE and FEIE, the FTC directly reduces your U.S. tax liability.

Knowing your total foreign earned income is crucial as it affects your overall tax obligations and eligibility for various exclusions and credits.

Using the FTC can further reduce your U.S. tax bill, especially if your foreign taxes are higher than the U.S. taxes.

Example scenarios illustrating the use of FTC

- Scenario 1: An expatriate in France pays $20,000 in French taxes on their income. They can use the FTC to reduce their U.S. tax liability by the same amount.

- Scenario 2: An expatriate in Brazil earns $80,000 and pays $15,000 in Brazilian taxes. They can use both the FEIE and FTC to minimize their U.S. taxes.

Opportunities to save on state taxes

Most U.S. states impose state income taxes on residents' earnings, even if they are living abroad. This means that, in addition to federal taxes, you could be paying state taxes on your income, which can significantly reduce your overall earnings.

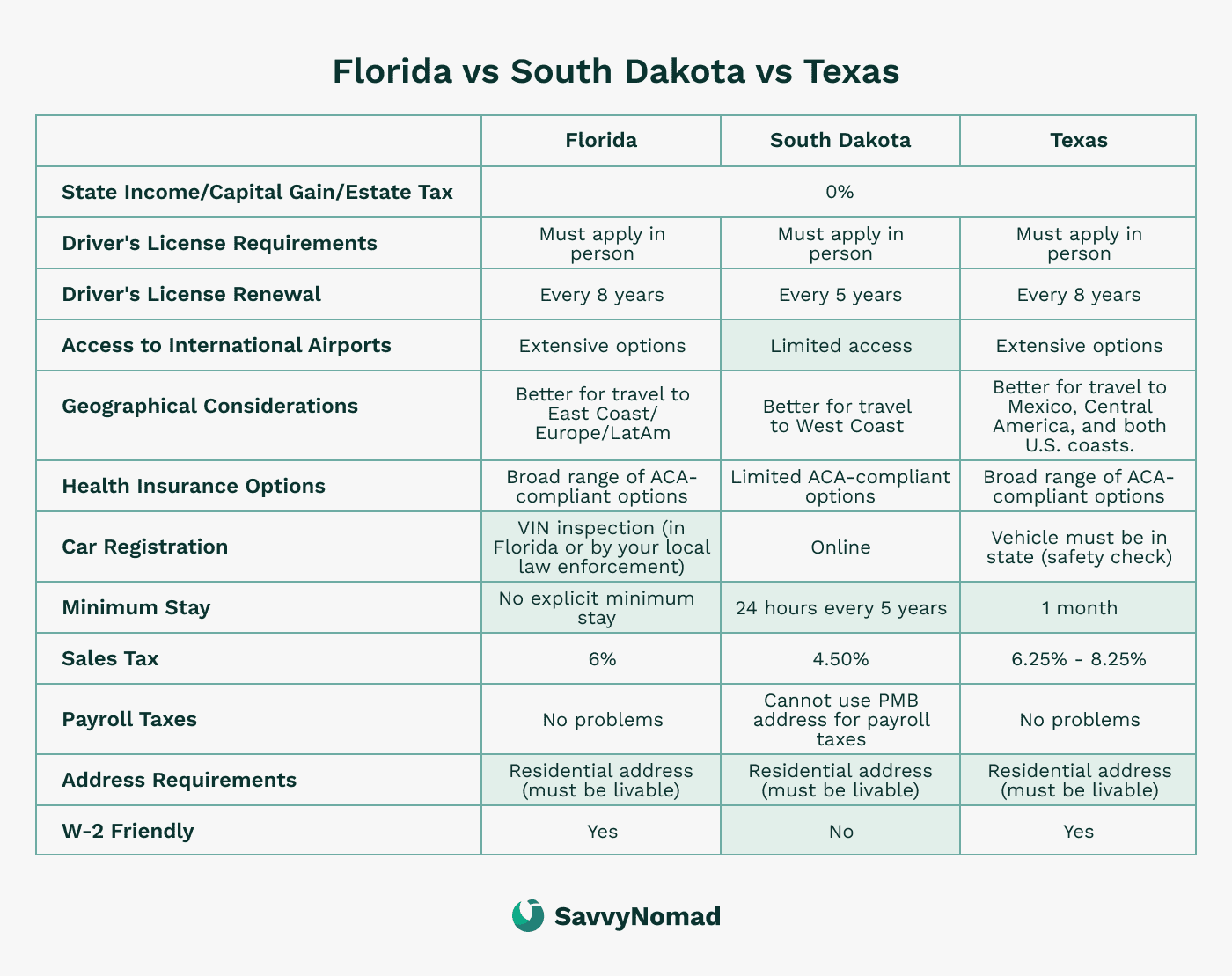

By changing your domicile to a state with no state income tax, such as , Texas, or South Dakota, you can avoid paying state income taxes. This can lead to substantial savings, especially if you are earning a high income while living abroad.

Process of changing domicile:

- Establish residency in the new state: This involves getting a driver's license, registering to vote, and possibly buying or renting a home in the new state. SavvyNomad can assist you with establishing residency by providing guidance and resources tailored to your needs.

- Move your financial accounts and other important records: Transfer your bank accounts, insurance policies, and other important documents to the new state.

- Sever ties with your previous state of residence: This includes closing accounts, ending leases, and changing your mailing address.

Changing your domicile to a no-tax state can result in significant state tax savings, which can add to the benefits you already receive from FHE, FEIE, and FTC. This means more of your income stays in your pocket, rather than going to state taxes.

Examples of tax savings by relocating domicile:

- Example 1: An expatriate moving from a high-tax state like California to a no-tax state like Florida could save thousands of dollars annually in state income taxes. If the expatriate earns $100,000 annually, and California's state income tax rate is 10%, they could save $10,000 each year by relocating to Florida.

- Example 2: An expatriate living abroad who relocates their domicile from New York to South Dakota might save around $8,800 annually, considering New York’s state income tax rate of approximately 8.8%.

How SavvyNomad can help

SavvyNomad specializes in assisting American nomads and expatriates with domicile transitions to tax-friendly states.

Our services include:

- Legal Address and Residency Filing: Helping you establish a legal address and register for residency in states with no income tax.

- Personalized Customer Support: Offering guidance on moving your financial accounts, closing ties with your previous state, and ensuring all paperwork is correctly filed.

- Mail Forwarding and Digital Mail Scanning: Providing solutions to manage your mail efficiently, no matter where you are in the world.

- Compliance Monitoring: Ensuring you remain compliant with state and federal regulations throughout the domicile transition process, providing peace of mind that all legal and tax requirements are being met.

FAQ

What is the maximum foreign housing exclusion?

For the 2024 tax year, the maximum foreign housing exclusion is $37,950. This amount is calculated as 30% of the Foreign Earned Income Exclusion (FEIE), which is set at $126,500 for 2024.

Here's a detailed breakdown:

1. Base Housing Amount: This is 16% of the FEIE. For 2024, this base amount is $20,240 ($126,500 * 0.16). This base housing amount represents the portion of your housing expenses that you cannot exclude.

2. Maximum Housing Exclusion: This is the upper limit of housing expenses you can exclude from your taxable income. It is set at 30% of the FEIE. For 2024, the maximum housing exclusion is $37,950 ($126,500 * 0.30).

Calculation Example:

- Qualifying Housing Expenses: Suppose you have $30,000 in qualifying housing expenses for the year.

- Base Housing Amount: $20,240

- Excess Housing Expenses: $30,000 $20,240 = $9,760

- Maximum Housing Exclusion: Since $9,760 is less than the maximum limit of $37,950, you can exclude the full $9,760 from your taxable income.

Additionally, if you live in a high-cost location identified by the IRS, the maximum limit can be adjusted to reflect higher local housing costs. These adjusted limits can be found in IRS guidelines.

Can both spouses claim the foreign housing exclusion?

Yes, both spouses can claim the Foreign Housing Exclusion if they both qualify as individuals under the tax rules.

Here’s how it works:

- Different Residences: If spouses live apart and have different tax homes, both can exclude their respective housing costs.

- Separate Returns: If they file separate returns, they must compute their housing costs separately, but can allocate expenses between them.

- Joint Return: If both spouses reside together and file a joint return, they can choose to compute their housing cost amount either jointly or separately. However, only one spouse can claim the exclusion if computed jointly.

What is the difference between foreign housing exclusion and deduction?

The Foreign Housing Exclusion and the Foreign Housing Deduction both allow U.S. taxpayers living abroad to reduce their taxable income by accounting for housing expenses, but they apply in different situations:

Foreign Housing Exclusion:

- Available to employees.

- Allows exclusion of qualified housing expenses from taxable income.

- Filed using Form 2555.

Foreign Housing Deduction:

- Available to self-employed individuals.

- Allows deduction of qualified housing expenses from taxable income.

- Filed using Form 2555.

Both options reduce taxable income but are tailored to different types of income earners.