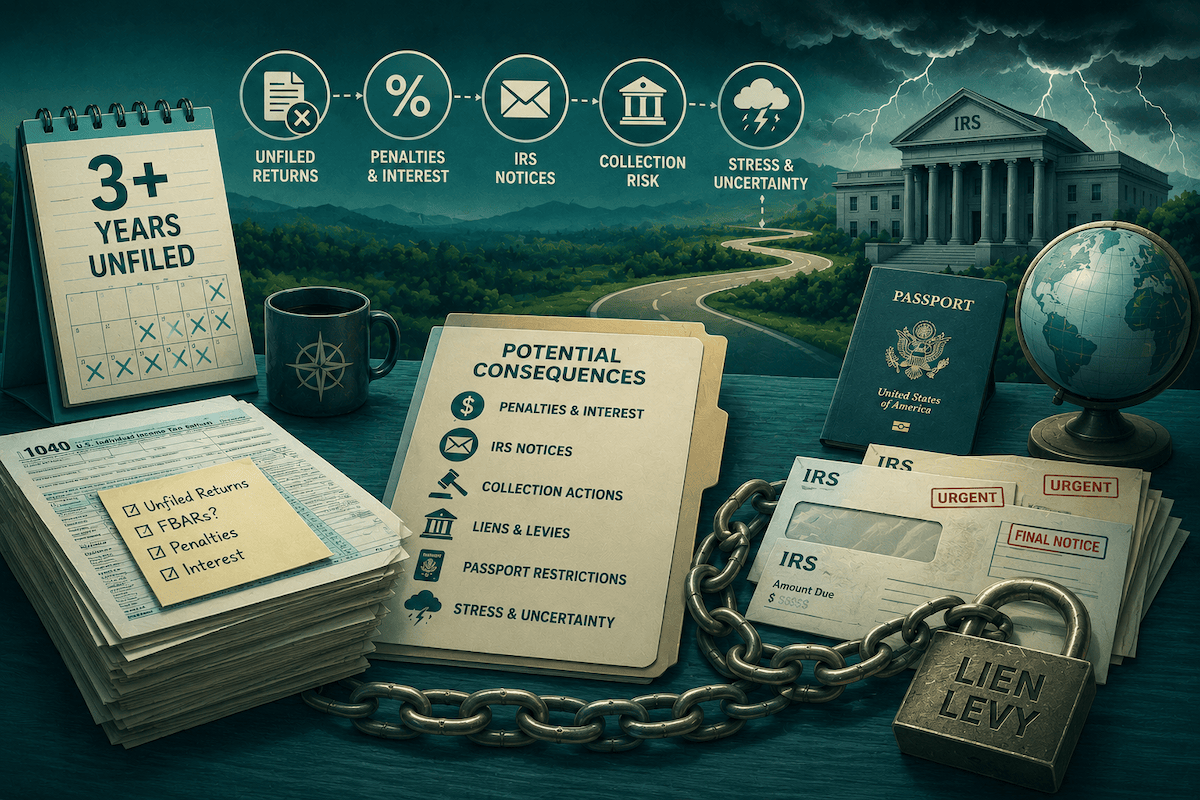

What happens if I haven't filed taxes in 3+ years

Haven't filed US taxes in 3+ years? The situation is fixable, but penalties compound monthly for every unfiled year, and the most favorable IRS compliance programs close the moment the IRS contacts you. Here's exactly what you're facing and how to resolve it.

If you haven't filed US taxes for three or more years, the situation is fixable. That's the most important thing to know before reading anything else. The IRS has specific programs for exactly this scenario, including one designed for Americans abroad who didn't realize they had to file.

The reason to act now isn't that the IRS is about to knock on your door tomorrow. It's because penalties compound monthly, interest accumulates daily, and the compliance options available to you before the IRS contacts you are significantly more favorable than the ones available after.

The window for the most accessible programs can also close without warning; as of July 1, 2026, the IRS quietly eliminated one long-standing penalty-relief program with no prior notice.

This article covers what you're actually facing, how the IRS finds non-filers, the penalty math year by year, and the specific compliance pathway that most likely applies to your situation.

For most expats who simply didn't know about the US citizenship-based taxation requirement, the Streamlined Foreign Offshore Procedures are the most accessible path: file 3 years of delinquent returns plus 6 years of FBARs, certify non-wilfulness, and pay $0 in offshore penalties if living abroad. Because the Foreign Earned Income Exclusion and Foreign Tax Credit are available retroactively, many expats discover they owe little or no additional tax; the situation is a paperwork problem more than a tax liability problem. Without a filed return, the IRS statute of limitations never starts running; there is no year that simply ages out. Penalties compound monthly for every unfiled year. FBAR penalties are separate from and can exceed income tax penalties. As of July 1, 2026, the Delinquent FBAR Submission Procedures have been eliminated. The Streamlined program is now the primary route for most non-wilful non-filers with foreign accounts. Act before the IRS contacts you: once contact occurs, the most favorable compliance programs are no longer available.

The short answer: fixable, but the longer you wait the more it costs

The IRS is not in the business of criminalizing people who made an honest mistake. For Americans abroad who genuinely didn't know about the citizenship-based taxation requirement (and many people don't), because the US is one of only two countries in the world that taxes citizens on worldwide income regardless of where they live, so a legal resolution path exists and it's more accessible than most people fear.

What makes the situation worse over time is not the IRS discovering it. It's the mechanical accumulation of penalties and interest on every open year simultaneously. Three years of non-filing means three separate penalty calculations running in parallel, not sequentially. Every month you wait adds another month of failure-to-file penalties, failure-to-pay penalties, and daily compounding interest across all three years at once.

There is also a program-availability risk that didn't exist before. As of July 1, 2026, the IRS eliminated the Delinquent FBAR Submission Procedures, a long-standing program that allowed certain taxpayers to file late FBARs without penalty. It was ended without prior public notice. The Streamlined Foreign Offshore Procedures remain available, but the trend is clearly toward fewer options over time, not more. Taxpayers who qualify for the remaining programs should not assume they will still be available next year.

What happens if you don't file US taxes while living abroad

Taxes on American citizens living abroad

What the IRS actually knows and how non-filers get found

The IRS is not tracking every American abroad in real time. But it has significantly more information sources than most non-filers realize, and more of those sources have become automated over the past decade.

- W-2s, 1099s, and information returns. Employers and US financial institutions file information returns with the IRS regardless of whether the taxpayer files their own return. If you received US-source income, salary from a US employer, dividends from a US brokerage, consulting fees from a US company, the IRS has a record of it.

- FATCA cross-referencing. Foreign financial institutions report US account holders to the IRS under FATCA. The IRS has records of many Americans' foreign accounts even if no FBAR was ever filed. This is what makes "I just won't mention the foreign account" a significantly riskier strategy than it was a decade ago.

- IRS CP59 notices. The IRS sends automatic notices to people who appear to have a filing obligation based on information returns but haven't filed. If you have a US address on file or a Social Security number that appears on information returns, you may already have received one or be receiving one.

- The passport denial program. Under IRC #7345, the IRS can certify seriously delinquent tax debt to the State Department, which can then deny passport applications or revoke existing passports. This is an increasingly used enforcement mechanism that directly affects Americans living abroad, a passport denial is how many non-filers first discover the IRS has found them.

The most important legal point: without a filed return, the statute of limitations on assessment never starts running. The IRS can assess tax on an unfiled year at any time, indefinitely. There is no point at which an unfiled year simply ages out. This is fundamentally different from the 3-year audit window that applies to filed returns.

The penalty math: how 3 years of non-filing compounds

Most people who haven't filed significantly underestimate what three years of accumulated penalties actually looks like. Here's the structure.

Failure-to-file penalty

5% of unpaid tax per month, up to 25% maximum per year. If the return is more than 60 days late, the minimum penalty is the lesser of $510 (2026) or 100% of the tax due. This is applied separately to each unfiled year.

Failure-to-pay penalty

0.5% of unpaid tax per month, up to 25% maximum. Both penalties can run simultaneously, with a combined effective cap of 47.5% of unpaid tax. The failure-to-pay rate reduces to 0.25% per month once a payment plan is agreed.

Interest

Compounds daily on unpaid tax and accrued penalties at the federal short-term rate plus 3 percentage points, currently approximately 8% annually. There is no cap; it continues until the full balance is paid.

How three years looks in practice

Consider an illustrative scenario: a US expat with $5,000 in US tax owed per year, across three unfiled years. The original tax liability is $15,000. After three years of failure-to-file penalties reaching their 25% cap, that's up to $3,750 in penalties per year: $11,250 in penalties alone.

Add daily compounding interest on the growing balance across all three years simultaneously, and total exposure could reach $30,000 or more, depending on timing. The penalties and interest can easily match or exceed the original tax owed.

FBAR penalties, the separate, potentially much larger number

FBAR penalties are calculated entirely separately from income tax penalties and are governed by different rules.

For a non-wilful FBAR violation, the penalty can reach $16,536 per annual report in 2026. Following the 2023 Supreme Court decision in Bittner v. United States, non-wilful penalties apply per annual FBAR report, not per account. This is important: an expat with three foreign accounts who failed to file one FBAR for one year owes up to $16,536 for that year's report, not $16,536 per account.

For a wilful FBAR violation, the penalty is the greater of $165,353 or 50% of the highest account balance for that year, per year. The difference between non-wilful and wilful is enormous.

For many expats, the FBAR exposure exceeds the income tax liability. This is why the available compliance programs, which waive or replace these penalties with a far smaller amount, are worth using.

Your compliance options

The most important rule: all favorable compliance options require you to act before the IRS contacts you. Once the IRS initiates a civil examination or contacts you about delinquent returns, the Streamlined program is no longer available.

| Feature | Streamlined Foreign Offshore (SFOP) | Voluntary Disclosure Program (VDP) | Late Filing (Quiet Disclosure) |

|---|---|---|---|

| Who it's for | Non-wilful non-filers living outside the US | Wilful non-filers or those with criminal exposure | Minimal amounts, no foreign accounts, low risk |

| Residency requirement | Must have lived outside the US during the non-compliance period | No residency requirement | No residency requirement |

| Returns required | 3 years of delinquent returns | Generally 6 years | All delinquent years |

| FBARs required | 6 years | Generally 6 years | All delinquent years |

| Income tax penalties | Waived | Civil fraud penalty may apply (75% on one year) | Full penalties apply |

| FBAR penalties | Waived if submission is complete | Generally one wilful penalty under examiner discretion | Full penalties apply |

| Offshore penalty | $0 (for non-residents) | Higher — determined case by case | N/A |

| Criminal protection | No formal protection | ✅ Yes — primary benefit of VDP | ❌ No |

| Requires IRS contact? | Must act before IRS contact | Must act before criminal investigation | No requirement |

| Best for most expats? | ✅ Yes | Only if wilful or high-risk | Rarely — get advice first |

Streamlined Foreign Offshore Procedures, for most expats reading this article

Who it's for: US citizens and Green Card holders who were living outside the US during the period of non-compliance and whose failure to file was non-wilful — due to negligence, inadvertence, mistake, or a good-faith misunderstanding of the law.

What it requires: File 3 years of delinquent federal tax returns, submit 6 years of delinquent FBARs electronically through the FinCEN BSA E-Filing System, complete Form 14653 (non-wilfulness certification), and mail the full package (tax returns and certification only — not the FBARs, which go separately) to the IRS Streamlined processing address. Write "Streamlined Foreign Offshore" in red at the top of each submitted return.

What it costs: $0 in the Title 26 miscellaneous offshore penalty for eligible non-residents. No failure-to-file, failure-to-pay, accuracy-related, or FBAR penalties if the submission is complete and non-wilfulness is accurate. You pay any back tax owed plus interest — and for many expats, the FEIE and Foreign Tax Credit applied retroactively eliminate most or all of the back tax.

The non-wilfulness certification is a legal document signed under penalties of perjury. If the IRS later determines the non-compliance was wilful, using the Streamlined program does not provide protection — and the certification itself becomes a problem. If there is any question about whether your situation was truly non-wilful, get professional advice before certifying.

IRS Voluntary Disclosure Program (VDP), for wilful situations or criminal exposure

Who it's for: Taxpayers with wilful non-compliance, potential criminal exposure, or situations too complex or large for the Streamlined program. The VDP involves higher penalties and a more structured multi-year disclosure process, but it provides protection from criminal prosecution.

Key point: the VDP must be entered before the IRS initiates an investigation. Once you're under investigation, this option closes.

Late filing without a program ("quiet disclosure")

What it is: Simply filing the missing returns without using a formal program.

The risks: provides no protection from penalties, no protection from prosecution, and the IRS has explicitly stated that quiet disclosures outside the Streamlined program may be selected for audit and subjected to full penalties. For anyone with foreign accounts or significant tax owed, this is rarely the right approach.

Decision framework:

- Living abroad, didn't know you had to file, non-wilful - Streamlined Foreign Offshore

- Wilful, large amounts, potential criminal exposure - VDP

- Minimal amounts, no foreign accounts, no IRS contact, professional advice confirms low risk - possibly late filing, but verify first

Special considerations for expats who didn't know they had to file

This is where the situation for most SavvyNomad readers is meaningfully different from domestic tax evasion, and where the law specifically recognizes that difference.

The citizenship-based taxation system is genuinely unusual. Most countries tax residents, not citizens. An American who moves to the Netherlands and pays Dutch taxes may have no idea that the US still expects a return. This is the factual foundation for a non-wilful classification, and it is a classification the IRS created the Streamlined program to accommodate.

Non-wilfulness is a legal standard: the failure to comply was due to negligence, inadvertence, mistake, or a good-faith misunderstanding of the law. An American who moved to Japan at 28, opened a Japanese bank account, and filed Japanese taxes dutifully for five years while never filing a US return because nobody mentioned that this was still required, that is a textbook non-wilful case.

The FEIE retroactivity rule removes most of the financial fear: the Foreign Earned Income Exclusion can be claimed on late returns for the years in which it would have applied. For 2024, the FEIE exclusion amount is $126,500; for 2025, it's $130,000 (verify 2026 at the time of publishing). Most expats earning below these thresholds owe zero or minimal additional US tax on their delinquent returns, even after three or more years. The non-filing was a paperwork failure, not a tax liability problem.

The Foreign Tax Credit can further reduce or eliminate any remaining liability by crediting taxes already paid to the country of residence. In many cases, expats going through Streamlined Offshore file three years of returns, claim FEIE or FTC, owe $0 in back tax, and pay only the professional fees to prepare and file the returns.

One SavvyNomad client, an IT Chief managing US state requirements from overseas, described what the uncertainty of unresolved compliance feels like:

"Managing state requirements from thousands of miles away can feel like trying to solve a puzzle without all the pieces. There was always a lingering uncertainty in the background. After transitioning with SavvyNomad, that stress disappeared."

For three-year non-filers, that "lingering uncertainty" often describes the situation precisely. The fix is available. The uncertainty is what's optional.

The refund trap: expired years can't be recovered

A consequence most readers don't anticipate: a return filed more than 3 years after the original due date cannot claim a refund, even if the taxpayer overpaid or was owed one.

If you had US withholding taken from a US-source payment, or paid estimated taxes, or had a refundable tax credit, and you were owed a refund for years you didn't file, that money is permanently forfeited once the 3-year window has passed. The Streamlined program allows you to come into compliance and eliminates penalties, but it does not recover expired refund claims.

This is not a reason to continue waiting. Every month that passes closes another potential refund window. It's a reason to file now rather than later.

Frequently asked questions

Will the IRS audit me if I file late through the Streamlined program? Returns submitted under Streamlined are processed like regular returns and may be selected for audit through normal processes. However, if selected, you cannot be assessed accuracy-related penalties, information return penalties, or FBAR penalties based on the Streamlined submission — unless the IRS determines the original non-compliance was fraudulent or wilful.

Can I claim the FEIE on late returns? Yes. The Foreign Earned Income Exclusion can be claimed retroactively on delinquent returns for the years it applied. For many expats, this eliminates most or all of the back tax owed. Foreign Earned Income Exclusion

What if I can't afford to pay what I owe? Filing the returns without paying is significantly better than not filing at all: the failure-to-file penalty (5% per month) is worse than the failure-to-pay penalty (0.5% per month). The IRS also offers instalment agreements and currently-not-collectible status. Get professional advice on payment options.

Can I get penalties waived without using the Streamlined program? The reasonable cause defense applies to income tax penalties for taxpayers who can demonstrate reasonable cause and lack of wilful neglect. This is separate from the Streamlined program and may be worth exploring with a tax professional in specific circumstances.

Do I need a CPA, or can I do this myself? For 3+ years of unfiled returns with foreign accounts, professional assistance is strongly recommended. The non-wilfulness certification is signed under penalties of perjury and involves legal judgments about the characterization of past conduct. Getting it wrong has more serious consequences than the cost of professional help.

What if I had no income, do I still need to worry? Possibly. FBAR is required regardless of income if foreign account balances exceeded $10,000 at any point. FATCA reporting thresholds also apply regardless of income. For income tax, if your income was below the filing threshold for each year, no income tax return was required. But the FBAR and information return obligations may still exist, and the passport denial program applies to tax debt, not necessarily to non-filers with zero income.

Conclusion

Three years of unfiled returns is a solvable problem. The Streamlined Foreign Offshore Procedures provide a defined, accessible path for non-wilful expat non-filers — one that waives penalties entirely and, for most expats, results in little or no back tax owed once FEIE and Foreign Tax Credit are applied retroactively.

What makes the situation compound is waiting. Penalties accumulate monthly. Interest accrues daily. Compliance programs have already begun to disappear; the Delinquent FBAR Submission Procedures were eliminated on July 1, 2026, without prior notice. The Streamlined program remains available, but its continued existence is not guaranteed.

The best time to act was when you first realized there was a problem. The second-best time is now, before the IRS contacts you and the most favorable options close.

SavvyNomad's CPA-access service connects you with cross-border tax professionals experienced in late filing, Streamlined submissions, and expat compliance.