Must Expats from New York Continue to Pay State Taxes?

New York’s nuanced tax laws make navigating state taxes complex for New York expats. Understanding residency status and tax obligations can have big consequences because New York's tax liabilities can extend globally while you may be living abroad.

Compliance with New York’s domicile rules and laws is necessary to avoid unexpected legal and financial consequences (remember, ignorance of the law is no excuse for breaking it!). This knowledge helps you adhere to the law and assists expatriates living their best lives abroad in efficient financial planning.

TLDR:

If you haven't established a new domicile in another state, you may still be considered a New York resident for tax purposes (even if you haven’t been there all year).

Understanding your residency status in NY

In New York State, your residency status significantly influences your tax obligations. There are three main residency statuses: resident, nonresident, and part-year resident. Each status has its own distinct criteria and tax implications.

Resident

You're considered a resident if New York is your domicile, meaning it's your permanent home—the place you intend to return to after absences. Additionally, if you maintain a dwelling in New York for more than 11 months and spend at least 183 days in the state within the tax year, you're deemed a resident. Residents are taxed on their worldwide income, regardless of where (and how) it's earned.

Nonresident

Nonresidents are those who do not meet the criteria to be considered residents. You might work in New York or earn income from New York sources but live elsewhere, like New Jersey or Connecticut, as common examples.

Nonresidents are taxed only on income earned from New York sources, such as wages for work performed in New York or income from property located in New York.

Part-year resident

If you move to or from New York during the tax year, you might be classified as a part-year resident. This status applies if you change your permanent home from New York to another location or vice versa.

Part-year residents are taxed on all income received, while a resident and New York-source income is received only during the portion of the year they were nonresidents.

For those who moved abroad

If New York was your last state of residency before moving abroad, you might still have tax filing obligations to consider, even if you no longer live there. New York employs a " domicile " concept to determine tax residency, which is more complicated than where you spend your time.

If New York was your domicile and you haven't established a new one in another state or country, you may still be considered a New York resident for tax purposes, meaning you are subject to New York taxes.

New York’s 548-day foreign-assignment safe harbor (temporary nonresident rule)

- During a period of 548 consecutive days, you are present in one or more foreign countries for at least 450 days; and

- During that same 548-day period, you, your spouse (unless legally separated), and your minor children spend 90 days or fewer in New York State; and

- During the nonresident portions of the tax years in which the 548-day period begins and ends, your days in New York do not exceed the prorated 90-day limit in the statutory formula.

When you meet the rule precisely and maintain solid documentation, New York examiners generally respect it in practice. However, it does not change your domicile—it only provides temporary nonresident protection for the qualifying period. It’s best suited to clearly defined foreign assignments with an end date; if your move abroad is long-term or entrepreneurial (not a formal employer assignment), it’s usually lower-risk to end New York domicile entirely by establishing domicile in another state first (e.g., Florida).

It’s best suited to clearly defined foreign assignments with an end date; if your move abroad is long-term or entrepreneurial (not a formal employer assignment), it’s usually lower-risk to end New York domicile entirely by establishing domicile in another state first (e.g., Florida).

What examiners look for: passport stamps and travel logs; your employment contract and employer verification; foreign housing leases; and consistent records showing you did not maintain a NY permanent place of abode.

What constitutes New York-sourced income?

New York-sourced income includes, but is not limited to:

- Wages and Salaries: Money earned for services performed in New York State, regardless of where your employer is based or where you reside.

- Capital Gains: Profits from the sale of real estate or tangible property located in New York State.

- Business Income: Income from business activities conducted in New York State, including partnerships and sole proprietorships.

- Real Estate: Rental income from property located within New York State.

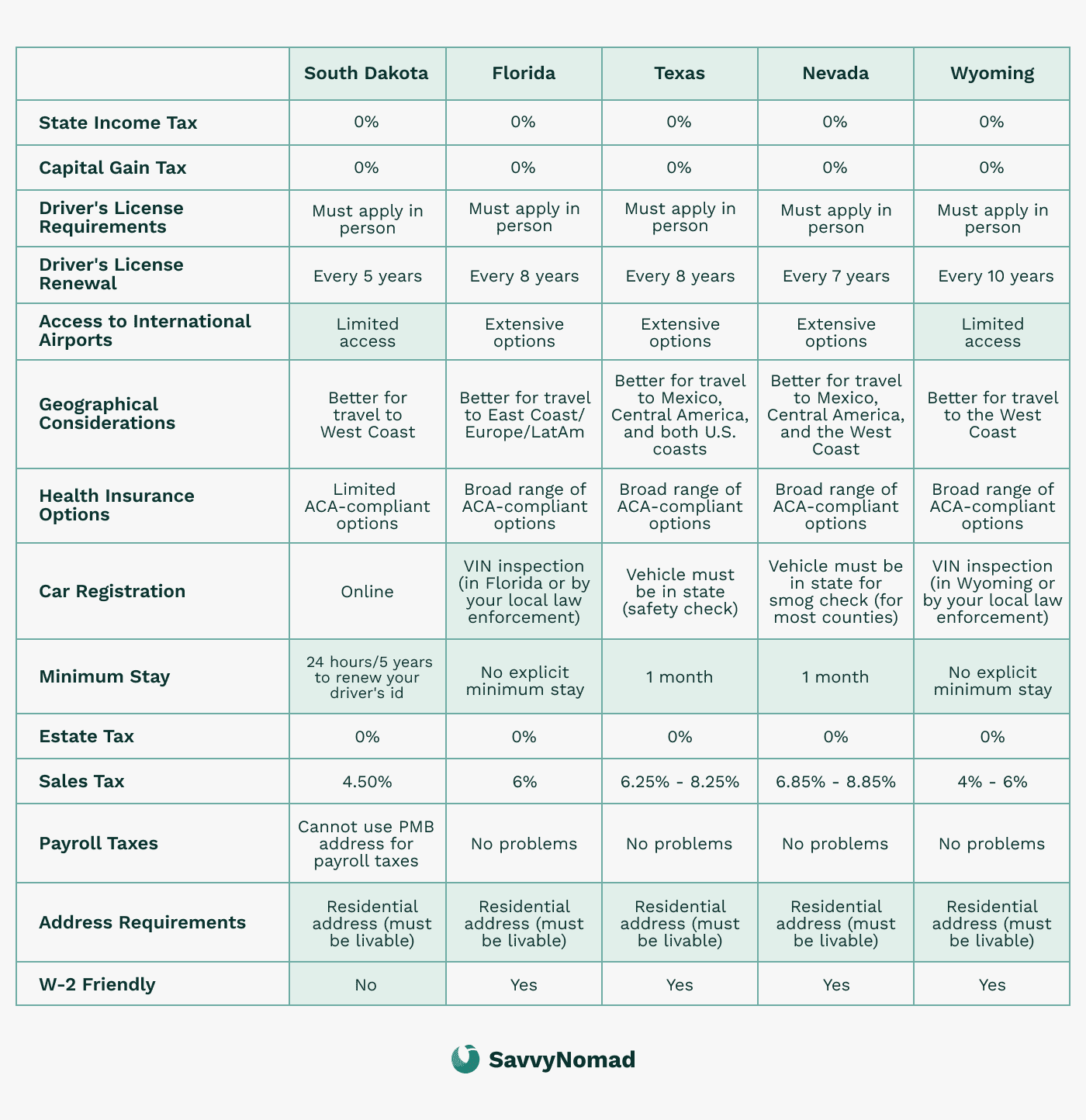

Why should you move domicile to a state with zero state income tax?

State income tax savings

For retirees and high-income individuals living in New York, moving to states without income taxes, such as Florida, Texas, or Nevada, can offer significant financial advantages. Without the burden of state income taxes, you can keep more of your earnings, allowing for greater investment opportunities or an enhanced lifestyle.

Inheritance tax benefits

States like Florida and Texas lack a state income tax and do not impose state estate taxes. This can considerably reduce the tax burden on your estate, which may help more wealth be passed on to your heirs. This is especially advantageous for individuals with substantial assets who wish to maximize the amount left to their beneficiaries.

Flexibility and mobility

Relocating your domicile to a no-income-tax state enhances your flexibility and mobility, allowing you to travel and live in various locations without worrying about high state tax bills.

This is ideal for high-income earners with business interests in multiple states or countries and for retirees who desire to spend their later years exploring new places.

Moreover, the lack of state income taxes can simplify your tax filing process. In many cases you may only need to file federal taxes, reducing the complexity and potential for errors in your tax returns and making financial management more straightforward. Depending on your situation, you could still have filing obligations in other states (for example, where you earn source income).

Foreign domicile vs. moving to another U.S. state

Establishing foreign domicile is often more documentation-intensive than moving your domicile to another U.S. state. Expect immigration/residency permits, foreign lease or deed, local tax ID, banking/ID changes, and more.

New York applies high scrutiny to intent and documentation, so if your plan is indefinite or long-term, it’s typically simpler (and easier to defend on audit) to end New York domicile by establishing domicile in a no-tax U.S. state (e.g., Florida) rather than trying to prove domicile in a foreign country.

Once your new U.S. domicile is clearly established, you won’t need to monitor foreign-assignment day-counts, and domicile-related audits usually become more straightforward to defend.

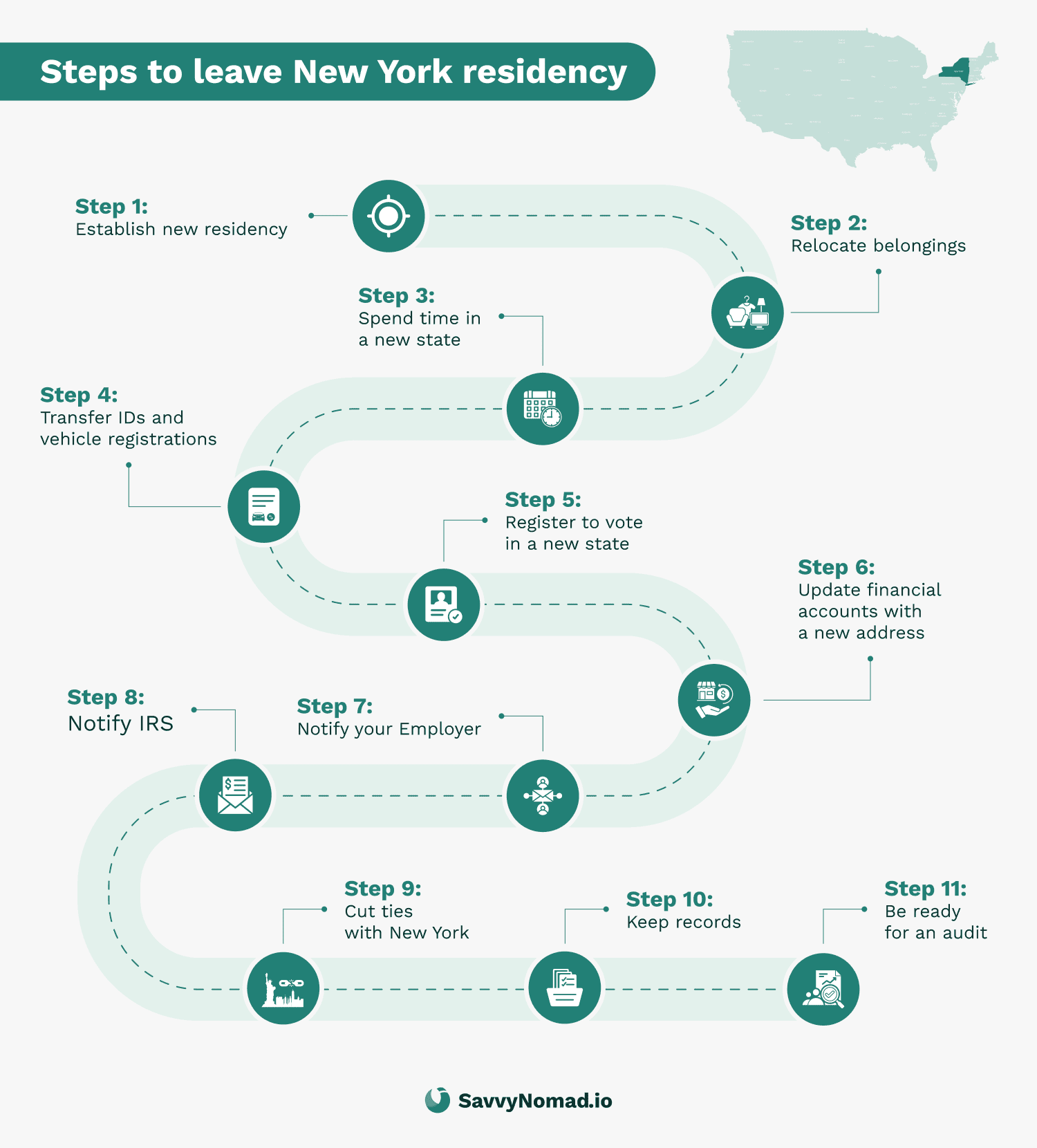

How to leave New York state tax residency?

Changing your New York State residency involves several calculated steps to help make the transition as clear-cut as possible.

1) Establish new residency

Secure a residential address in the new state. If you buy a home, you may want to look into available tax credits, such as Florida’s homestead exemption. You may want to consider filing a Declaration of Domicile with the state, as suggested in Savvy Nomad’s domicile guides.

The address is provided solely for documentary and correspondence purposes related to client-direct banking or brokerage verification; it is not for business registration, public listing, or mail forwarding. Banks and state agencies make their own decisions, no specific outcome is guaranteed, and prior-state rules may still apply.

2) Transfer IDs and registrations

Promptly update your driver's license and vehicle registration as soon as you are eligible.

3) Register to vote (if eligible)

If you are eligible, you may register to vote in your new state. Voter registration is one supporting indicator of domicile—not determinative on its own. For eligibility and procedures, consult election officials in your new state.

4) Update documents

Make sure that all identification, medical, insurance and financial documents reflect your new address.

5) Notify your employer

It’s important to notify your employer of your residency change. This can also help convert some of your income from being “New York-sourced” if your employer recognizes that the work you complete is no longer done within NY state lines.

6) Notify IRS

Inform the IRS of your address change using Form 8822. Extend this notification to all personal and professional entities and, as soon as possible, engage professionals in your new state of domicile.

7) Keep records

Document all relocation actions diligently. Maintain records of flights, short- and long-term rentals, and travel dates. In the event of an audit, the burden of proof falls on the taxpayer to prove they are no longer a taxable resident of New York.

8) Acknowledge key factors

New York considers multiple factors for domicile status, including home, time spent within the state, business ties, location of valuables, and family location. Make sure you feel confident of as many of these as you can.

9) Anticipate an audit

Be audit-ready with comprehensive proof that your move to another state is permanent.

Tax benefits and exemptions for expats from New York

Living abroad as an expat comes with various federal tax benefits and exemptions that can help reduce your overall tax burden.

Here are some of the key federal tax advantages available:

Foreign Earned Income Exclusion

The FEIE allows U.S. taxpayers living abroad to exclude a certain amount of their foreign-earned income from U.S. federal income tax.

For the tax year 2024, this exclusion amount is up to $126,500.

To qualify, you must pass either:

• Bona Fide Residency Test: You qualify if you are a resident of a foreign country for an uninterrupted period that includes an entire tax year.

• Physical Presence Test: You qualify if you are physically present in a foreign country for at least 330 full days during a 12-month period.

Foreign Tax Credit

The foreign tax credit (FTC) helps you avoid double taxation by allowing you to credit foreign taxes paid against the U.S. federal taxes due on income that is also subject to U.S. federal tax.

This credit can significantly reduce your U.S. tax liability, especially if you reside in a country with high tax rates.

State credits are separate from the federal Foreign Tax Credit. New York’s resident credit generally applies to Canadian national/provincial income taxes only (it typically does not credit other countries’ taxes). To be allowed, you must show:

- The foreign levy is a net income tax (not a social contribution, wealth/solidarity levy, or general surcharge).

- The same income was taxed by the foreign jurisdiction and by New York (i.e., it’s truly double-taxed).

- Complete documentation: proof of payment, a copy of the foreign (and provincial, if applicable) return/assessment, translations if needed, and a tie-out schedule that links the foreign-taxed income to the same lines on your New York return.

Limits & interaction with the federal FTC: New York’s credit is generally capped at the New York tax on that double-taxed income. If you also claim the federal FTC on the same dollars, expect a state-level reduction—no double dipping.

Foreign Housing Exclusion (FHE)

Although its name uses the word “exclusion,” the FHE actually allows you to deduct certain housing expenses from your federal taxable income, including rent, utilities (excluding telephone), and other reasonable expenses related to housing abroad.

The amount you can deduct is limited to a base amount plus housing expenses exceeding 16% of the FEIE limit.

Filing New York state taxes from abroad

Filing New York State Taxes from abroad involves several important steps to help you stay compliant and avoid penalties.

Here's a streamlined approach:

1. Determine your residency status

First, establish whether you're considered a resident, nonresident, or part-year resident for the tax year. This status significantly influences your tax filing obligations.

2. Identify New York-sourced income

If you have income from New York sources—such as wages for work performed in the state, income from business operations conducted in New York, rental income from New York properties, or capital gains from the sale of property in New York—you may need to file.

3. Understand filing requirements

For Residents: If you were a resident of New York and are required to file a federal return, you likely will need to file a state return as well.

For Nonresidents: You must file Form IT-203 if your New York-sourced income exceeds your New York standard deduction or if you wish to claim a refund of New York State, New York City, or Yonkers income taxes withheld from your pay.

Additional filing requirements apply if you want to claim certain refundable or carryover credits or had a net operating loss for New York State personal income tax purposes.

4. Filing deadlines and forms

The typical deadline for filing New York State taxes is April 15. Expats are granted an automatic two-month extension, pushing back their deadline into June. Nonresidents and part-year residents should use Form IT-203, Nonresident and Part-Year Resident Income Tax Return.

5. Digital filing options

New York State offers e-filing services, which simplify the process for expatriates. These digital platforms guide you through filing and are designed to help you satisfy New York State’s requirements.

Penalties for non-compliance with New York state tax laws

Failing to adhere to New York State's tax obligations carries serious implications for both expatriates and former residents. The consequences of such non-compliance highlight the critical importance of maintaining tax obligations.

Implications of failing to meet state tax obligations

Non-compliance can lead to various penalties that underscore the necessity of staying informed and compliant with New York tax laws:

Fines and penalties

Neglecting to file or pay taxes on time can result in substantial fines. These penalties increase with the length of the delay, adding a significant financial burden to the taxes owed.

- Late filing and payment penalties: Failure to file or pay taxes by the deadline without reasonable cause incurs penalties. The penalties, which accumulate daily, are calculated based on the unpaid tax and the length of the delay.

- Underpayment penalty: Taxpayers who underreport their income face penalties and interest on the amount underpaid, which can significantly increase their tax liability.

Interest charges

Beyond fines, unpaid taxes accrue interest daily, further increasing the amount owed to the state.

Legal sanctions

In severe cases, such as tax evasion, the repercussions can extend beyond financial penalties to include legal action and possible criminal penalties.

Options for resolving tax issues

Recognizing the challenges that come with tax compliance, New York State provides mechanisms for taxpayers to address and resolve tax issues:

- Voluntary disclosure program: This initiative allows individuals who have failed to file or underreported their taxes to correct their tax affairs voluntarily. By making voluntary disclosure, participants can avoid criminal prosecution and may qualify for reduced penalties.

- Offer in compromise: Under certain conditions, taxpayers demonstrating financial hardship may be able to settle their tax debts for less than the full amount owed.

- Payment plans: For those unable to pay their tax debt in full, the state may offer payment plan options, facilitating manageable payments over an extended period.

FAQ

What triggers the NY residency audit?

New York residency audits can be triggered by high income, a change in domicile or statutory residency or, for many people, moving out of the state. Audits often begin with a questionnaire requesting proof of address.

Does New York have an exit tax?

No, New York has no official exit tax for residents leaving the state. However, residents who move out of New York during the tax year are generally required to file a part-year resident tax return and pay income taxes on any income earned while residing in New York.

Does New York have a 183-day rule?

New York uses a 183-day threshold as part of its statutory residency test, but it is not a stand-alone rule. A non-domiciliary is treated as a New York resident for income-tax purposes if they (1) maintain a permanent place of abode in New York for substantially all of the year and (2) spend more than 183 days in the state during the year. Both conditions must be met; day count alone is not enough.

What is the residency test in NYC?

The New York City residency test involves two main criteria: the Domicile Test and the Statutory Residency Test. Under the Domicile Test, an individual is considered a New York City resident for tax purposes if they are domiciled in New York City or maintain a permanent place of abode there and spend more than 183 days there.

On the other hand, the Statutory Residency Test deems an individual a resident if they maintain a permanent place of abode in the city for substantially all year and spend more than 183 days in New York City.

Can you leave residency and come back?

In a word, yes. Leaving New York residency and returning involves documenting your break from residency via a tax return, specifically Form IT-203, as a part-year resident.

The state considers several factors to determine residency, including domicile status, maintaining a permanent place of abode, and presence in the state for more than 183 days.

To reestablish residency, you would need to demonstrate a permanent move back to New York, considering factors like the location of your home, family, business, time spent in each state, and where you keep important possessions.