Do I have to pay NJ state taxes if I live abroad?

Understanding New Jersey’s tax obligations is important for expatriates with financial ties to the state. The tax laws in New Jersey are complex, especially when it comes to expat state taxes, and they hinge significantly on your residency status. Whether you’re a resident, a nonresident, or a part-year resident affects your tax responsibilities deeply.

For expats, this means navigating a landscape filled with intricate rules that dictate how your global income is taxed. In this introduction, we'll delve into why it's important for expats to grasp these complexities, helping them meet their legal requirements without facing unexpected tax burdens.

TLDR:

New Jersey usually treats you as a resident if New Jersey is your domicile, unless you (1) do not maintain a permanent home in New Jersey, (2) do maintain a permanent home outside New Jersey, and (3) spend 30 days or fewer in New Jersey during the year.

If you are a resident and over the state’s filing thresholds, you must file a New Jersey return and report your worldwide income.

Understanding residency status in New Jersey

Resident

Under New Jersey rules, you are a resident if New Jersey is your domicile, unless all of the following are true: you did not maintain a permanent home in New Jersey, you did maintain a permanent home outside New Jersey, and you spent no more than 30 days in New Jersey during the year.

You are also treated as a resident if New Jersey is not your domicile but you maintain a permanent home in New Jersey and spend more than 183 days in the state during the year. If New Jersey is your domicile, you are required to pay state taxes on all your income, no matter where it is earned.

This includes global income, which is taxed by New Jersey if it remains your primary home base.

Nonresident

Nonresidents are generally individuals who are not domiciled in New Jersey and do not spend more than 183 days in the state during the tax year.

In addition, a person who is domiciled in New Jersey can be treated as a nonresident if they do not maintain a permanent home in New Jersey, do maintain a permanent home elsewhere, and spend 30 days or fewer in New Jersey during the year.

They are only taxed on income that is sourced to New Jersey.

This includes earnings from work performed within the state, income from businesses located in New Jersey, or income from property situated in New Jersey. Nonresidents must use specific forms to declare and pay taxes on their New Jersey-sourced income.

New Jersey-Sourced Income

Income considered as sourced from New Jersey includes, but is not limited to:

- Wages and salaries: Money earned from employment performed in New Jersey.

- Business income: Income from business activities conducted in New Jersey, regardless of the business' location.

- Rental income: Income derived from property located within New Jersey.

- Capital gains: Profits from the sale of real estate or tangible personal property located in New Jersey.

Part-Year Resident

Part-year residents are those who either move to or from New Jersey during the tax year. This status requires individuals to file taxes as residents for the portion of the year they lived in New Jersey and as nonresidents for the remainder of the year. This allows them to appropriately allocate their taxable income based on where it was earned throughout the year.

Expatriates

Expatriates from New Jersey who still consider the state their domicile are required to pay state taxes on their worldwide income.

New Jersey law generally requires you to file a state tax return and report worldwide income if New Jersey remains your domicile and you do not meet the narrow nonresident exception (no New Jersey permanent home, permanent home elsewhere, and 30 days or fewer in the state).

This framework means your global income may be taxed by New Jersey as long as you are treated as a resident. Navigating expat taxes requires careful consideration of both state and federal tax laws so you stay compliant and avoid penalties.

Why should New Jersey expats move domicile to a state with zero state income tax?

State income tax savings

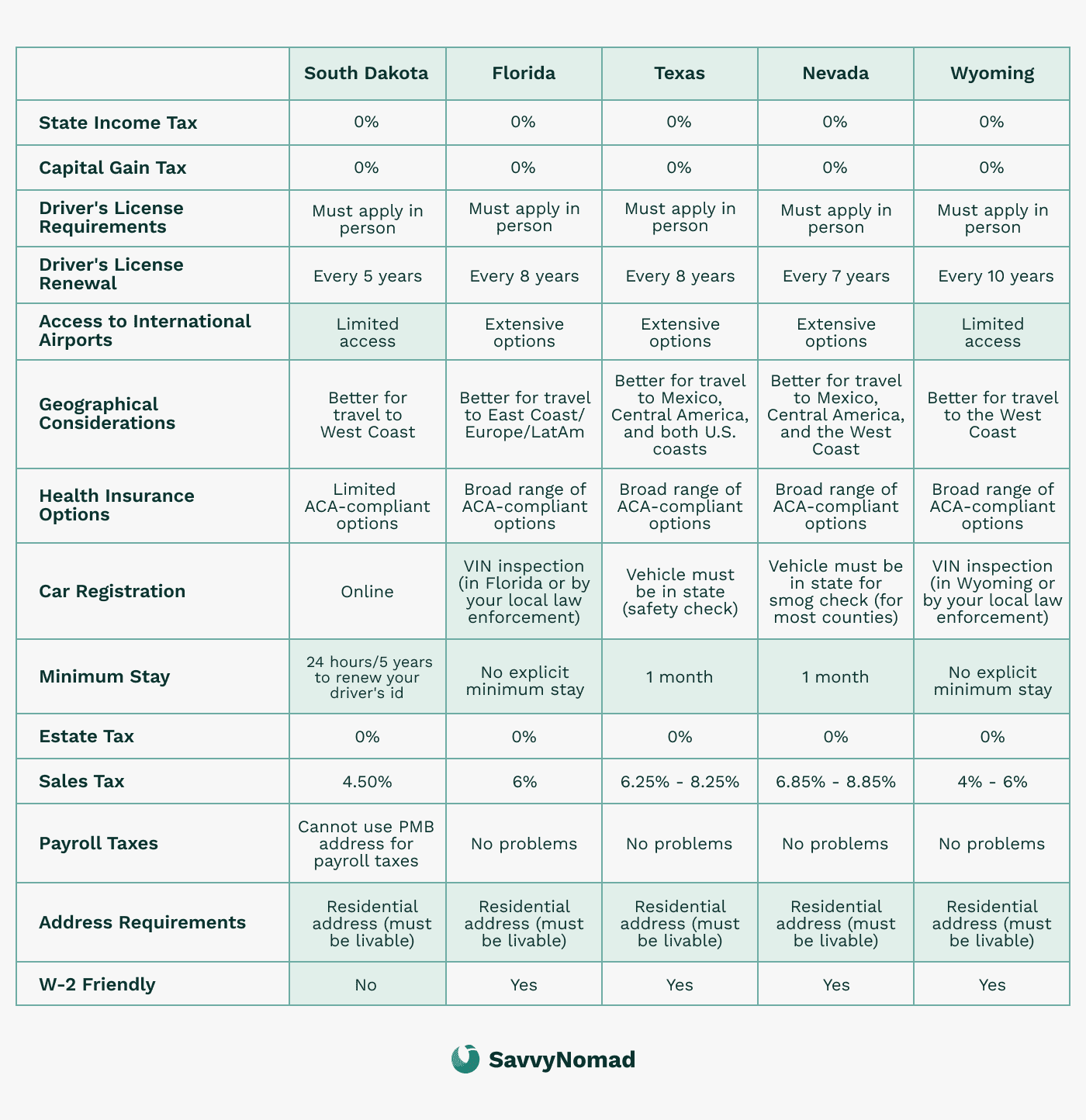

For retirees and high-income individuals from New Jersey, moving to states without income taxes, such as Florida, Texas, or Nevada, can offer significant financial advantages. This includes not only your salary but also other forms of income, such as investment income, which can be significantly impacted by state tax laws.

Without the burden of state income taxes, you can keep more of your earnings, allowing for greater investment opportunities or an enhanced lifestyle.

Inheritance tax benefits

States like Florida and Texas not only lack a state income tax but also do not impose state estate taxes. This can considerably reduce the tax burden on your estate, which may help more wealth be passed on to your heirs. This is especially advantageous for individuals with substantial assets who wish to maximize the inheritance for their beneficiaries.

Flexibility and mobility

Relocating your domicile to a no-income-tax state enhances your flexibility and mobility, allowing you to travel and live in various locations without worrying about high state tax bills. This is ideal for high-income earners with business interests in multiple states or countries and for retirees who desire to spend their later years exploring new places.

Moreover, the absence of state income taxes can simplify your tax filing process. In many cases you may only need to file federal taxes, reducing the complexity and potential for errors in your tax returns and making financial management more straightforward, though you could still have filing obligations in other states depending on your situation.

How to leave New Jersey tax residency?

Changing your New Jersey State residency involves several calculated steps to ensure a clear-cut transition.

1) Establish new domicile

Secure a residential address in the new state. You may want to consider filing a Declaration of Domicile with the state, as suggested in Savvy Nomad’s domicile guides:

The address is provided solely for documentary and correspondence purposes related to client-direct banking or brokerage verification; it is not for business registration, public listing, or general mail forwarding. Banks and state agencies make their own decisions, no specific outcome is guaranteed, and prior-state rules may still apply.

2) Transfer IDs and registrations

Swiftly update your driver's license and vehicle registration.

3) Register to vote (if eligible)

If you are eligible, you may register to vote in your new state. Voter registration is one supporting indicator of domicile, not determinative on its own. For eligibility and procedures, follow guidance from election officials in both states.

4) Update documents

Make sure all identification, medical, insurance, and financial documents show your new address.

5) Notify your employer

It's important to inform your employer about your change of residency, which can help in converting some of your income from "New Jersey-sourced".

6) Notify IRS

Inform the IRS of your address change using Form 8822. Extend this notification to all personal and professional entities.

7) Keep records

Document all relocation actions diligently.

8) Anticipate an audit

Be audit-ready with comprehensive proof of your move’s permanence.

Tax benefits and exemptions for New Jersey expats

Living abroad as an expat comes with various federal tax benefits and exemptions that can help reduce your overall tax burden. Here are some of the key federal tax advantages available:

Foreign Earned Income Exclusion (FEIE)

The FEIE allows U.S. taxpayers living abroad to exclude a certain amount of their foreign-earned income from U.S. federal income tax.

For the tax year 2024, this exclusion amount is up to $126,500.

To qualify, you must pass either:

- Bona Fide Residency Test: You qualify if you are a resident of a foreign country for an uninterrupted period that includes an entire tax year.

- Physical Presence Test: You qualify if you are physically present in a foreign country for at least 330 full days during a 12-month period.

Foreign Tax Credit (FTC)

The FTC helps you avoid double taxation by allowing you to take credit for foreign taxes paid on income that is also subject to U.S. federal tax.

This credit can significantly reduce your U.S. tax liability, especially if you reside in a country with high tax rates.

Foreign Housing Exclusion (FHE)

The FHE allows you to exclude certain housing expenses from your federal taxable income, including rent, utilities (excluding telephone), and other reasonable expenses related to housing abroad. The amount you can exclude is limited to a base amount plus housing expenses exceeding 16% of the FEIE limit.

Filing requirements for New Jersey expats

Filing state taxes from abroad can be straightforward once New Jersey expatriates understand the necessary steps and forms required to file state taxes based on their residency status and income sources.

Do I need to file a state tax return?

As a New Jersey expat, you may be wondering if you need to file a state tax return. The answer depends on your individual circumstances. If you are considered a resident of New Jersey, you are required to file a state tax return and report your worldwide income, including foreign income.

However, if you are a non-resident, you may only need to file a state tax return if you have income sourced to New Jersey.

To determine if you need to file a state tax return, you should consider the following factors:

- Your residency/domicile status: Are you a resident or non-resident of New Jersey?

- Your income: Do you have income sourced to New Jersey or foreign income that is subject to New Jersey state tax?

- Your tax obligations: Have you met your tax obligations in New Jersey and the federal government?

It’s essential to consult with a tax professional to determine your specific tax obligations and stay in compliance with New Jersey state tax laws. This will help you avoid potential penalties and make sure you’re meeting all your legal requirements.

How to file New Jersey state taxes from abroad:

1. Gather your documents

Before you begin the filing process, collect all pertinent financial documents. This includes worldwide income statements, proof of income from New Jersey sources, and any records of the days spent in New Jersey during the tax year.

2. Choose the correct form:

- NJ-1040: This is the form used by residents. As an expat, if you are considered a resident of New Jersey for tax purposes, you would use this form to report your global income. Understanding which form to use is crucial, as expats pay state taxes based on their residency status and income sources.

- NJ-1040NR: Nonresidents should use this form, which is designed to report income earned from New Jersey sources only.

- For part-year residents, the NJ-1040 form is used, and income must be allocated to the periods of residency and non-residency as applicable.

3. File electronically

New Jersey encourages taxpayers to file electronically for faster processing and quicker refunds. The state supports several e-filing services that expatriates can access from anywhere in the world.

4. Manual filing

If electronic filing is not an option, expatriates can also mail their tax returns to the New Jersey Division of Taxation. Be sure to use the correct mailing address, which varies depending on whether a payment is included with the return.

Penalties for non-compliance

Failing to meet tax obligations in New Jersey can lead to significant consequences, including various penalties and fines. Understanding these penalties can help you stay compliant and avoid unnecessary financial burdens.

Late filing and payment penalties

- Late filing: If you file your tax return after the due date and do not have an extension, New Jersey imposes a late filing penalty. The penalty is typically 5% of the tax due for each month or part of a month the return is late, up to a maximum of 25%.

- Late payment: If you pay your taxes late, the penalty is 0.5% per month on the balance due, up to a maximum of 25%. This penalty starts accruing the day after the tax is due until it is paid.

Underpayment of estimated tax penalty

If you do not pay enough through withholding or estimated tax payments, you may be subject to an underpayment penalty. This penalty applies if you owe more than a certain amount when you file your return. The penalty calculation is complex and depends on the amount underpaid and the period of underpayment.

Accuracy-related penalties

If your return shows an understatement of tax due to negligence or disregard of rules and regulations, New Jersey may assess an accuracy-related penalty. This can be significant, typically 10% of the underpayment attributable to the negligence.

Fraud penalties

In cases of tax fraud or intentional disregard of New Jersey tax laws, more severe penalties can be imposed. These penalties are much higher and may also lead to criminal charges.

Collection costs

If the state needs to take action to collect overdue taxes, such as through a levy or lien, the taxpayer can be charged additional fees and costs associated with the collection process.