Do expats from Utah still need to pay state taxes?

As an expat from Utah, it's important to understand your state tax obligations. Even if you live abroad, you might still owe taxes to Utah. Knowing whether you need to pay state taxes depends on two key factors: residency and domicile.

Residency is about where you currently live, while domicile is about where your permanent home is. Your tax responsibilities in Utah are determined by these factors. This article will help you understand how residency and domicile affect your tax obligations as an expat from Utah.

TLDR:

If Utah remains your domicile and you haven’t established residency in a different state, you are considered a Utah resident for tax purposes and must file state taxes on your worldwide income.

Utah calculates state taxes based on your federal adjusted gross income (AGI), so any foreign income excluded on your federal return will also be excluded from your Utah return.

The Foreign Earned Income Exclusion (FEIE) allows U.S. taxpayers living abroad to exclude up to $126,500 of foreign-earned income from their U.S. taxable income for the 2024 tax year.

This exclusion only applies to earned income, such as wages and salaries, and does not apply to passive income like interest, dividends, capital gains, and rental income.

To avoid state taxes, you must sever all ties with Utah and establish a new domicile in another state.

Understanding Utah's tax residency rules

Residency and domicile are critical in determining Utah tax obligations. Residency refers to where you live, while domicile is your permanent home where you intend to return after any absence.

Definition of residency and domicile

Residency: Residency is where you live, either temporarily or permanently. It is based on physical presence in a particular place.

Domicile: Domicile is your permanent home, the place you intend to return to and stay indefinitely. You can only have one domicile at a time, but you can have multiple residences.

You can reside in several places, but you can only have one domicile. Domicile requires intent to remain permanently

Resident

Domicile: You are considered a resident of Utah if your domicile, or permanent home, is in Utah. Your domicile is where you intend to return after any absences, whether temporary or long-term.

Physical Presence: If you spend more than 183 days in Utah during the tax year, you may be considered a resident for tax purposes, even if your domicile is elsewhere.

AGI and State Taxes: Utah calculates state taxes based on your federal adjusted gross income (AGI). Any foreign income excluded on your federal return is also excluded from your Utah return.

Nonresident

- No Domicile in Utah: You are a nonresident if your domicile is not in Utah and you do not maintain significant ties to the state.

- Limited Physical Presence: If you spend fewer than 183 days in Utah during the tax year, you may be considered a nonresident.

Nonresidents are only taxed on income originating from Utah sources, such as wages earned in Utah or income from property located in the state.

Part-Year Resident

Part-year residents live in Utah for part of the year and another state for the rest. They are taxed on all income earned while residing in Utah and only on Utah-sourced income during the non-resident part of the year

What constitutes Utah-sourced income?

Understanding what constitutes Utah-sourced income is essential for nonresidents and part-year residents to accurately determine your tax obligations.

Utah-sourced income refers to any income derived from activities or assets located within the state.

Here are some key categories to consider:

- Wages and Salaries: Money earned for services performed in Utah.

- Business Income: Income from business activities conducted in Utah.

- Real Estate: Rental income from property located in Utah.

- Capital Gains: Profits from the sale of real estate or tangible property in Utah.

- Dividends and Interest: Dividends from Utah-based companies and interest earned from Utah financial institutions.

- Pensions and Retirement Plans: Retirement income from Utah institutions or for services performed in the state.

Why should you move domicile to a state with zero state income tax?

State income tax savings

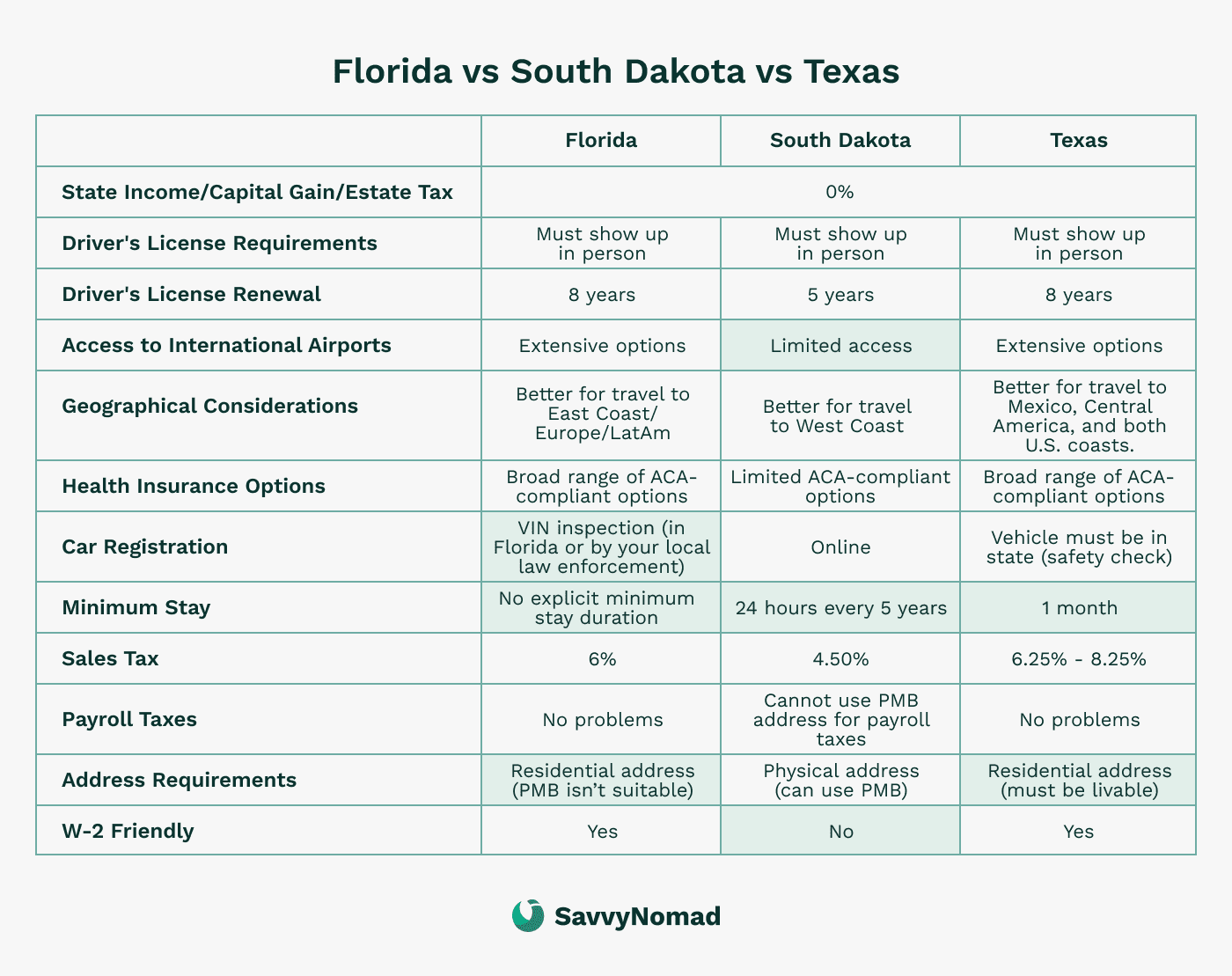

Retirees and high-income earners can greatly benefit from moving to states without state income taxes, such as Florida, Texas, and Nevada.

Without the burden of state income taxes, you can save more money, invest more, or enjoy a higher standard of living.

When income exceeds the Foreign Earned Income Exclusion (FEIE) limit of $126,500 in 2024, moving to a state with no income tax can be especially beneficial since it shields more of their income from state taxes.

Inheritance tax benefits

States with no income tax often have more favorable inheritance and estate tax laws. This can significantly benefit high-net-worth individuals by minimizing the tax liabilities on their estates, thereby preserving more wealth for their heirs

Flexibility and mobility

Moving domicile to a no-income-tax state enhances flexibility and mobility, allowing individuals to travel or live in multiple locations without worrying about high state tax bills. This is ideal for high-income earners who may have business interests in different states or countries and for retirees who wish to spend their golden years exploring new places.

Without state income taxes, your tax filing process becomes simpler. You only need to file federal taxes, reducing the complexity and potential errors in your tax returns.

How to leave Utah tax residency?

Here are the key steps to help you transition:

1) Establish new residency

- Secure a Residential Address: Obtain a residential address in your new state. This is the most critical step in establishing a new domicile. Consider using a domicile service that provides a residential address, assists with mail forwarding, and helps establish your new residency.

- File a Declaration of Domicile if required: Some states require a formal declaration to confirm your new domicile. This declaration typically includes an affidavit that you intend to make the new state your permanent home. Check the requirements of your new state and file the necessary documents to establish your intent to remain there permanently.

Reference guides may provide additional help for specific states:

2) Sever ties with Utah

- Sell property: If you own property in Utah, consider selling it or renting it out. Owning property can be a strong indicator of continued ties to the state.

- Transfer IDs and registrations: Update your driver’s license and vehicle registration to your new state. This demonstrates your commitment to establishing a new domicile.

- Register to vote: Register to vote in your new state. Voting registration is a strong indicator of your intent to establish residency.

- Update personal documents: Change your address on all identification cards, medical records, insurance policies, financial documents, and other important records.

3) Notify relevant parties

- Inform your employer: Notify your employer about your change of residency. This can affect how your income is taxed and helps establish your new domicile.

- Notify the IRS: Inform the IRS of your address change using Form 8822. Extend this notification to all personal and professional entities.

- Update all personal and professional entities: Inform banks, investment accounts, insurance companies, and other relevant entities about your change of address.

4) Keep detailed records

- Maintain documentation: Keep receipts, bills, lease agreements, and other legal documents that prove your new residency. Detailed records are essential if your residency status is questioned.

- Track your movements: Document your time spent in and out of Utah. This includes travel records, utility bills, and any other documents that show your physical presence in your new state.

5) Be prepared for audit

If the Utah Department of Revenue questions your residency status, be prepared to provide comprehensive proof that you have permanently moved out of Utah.

- Proof of permanent move: Be ready to provide comprehensive proof that you have permanently moved out of Utah, including all documentation showing that you have established a new domicile and severed ties with Utah.

- Respond to inquiries: If the Utah Department of Taxation questions your residency status, provide thorough responses and all necessary documentation promptly to avoid potential penalties.

Tax benefits and exemptions for expats from Utah

Living abroad as an expat from Utah comes with various tax benefits and exemptions that can help reduce your overall tax burden.

Here are some of the key tax advantages available:

Foreign Earned Income Exclusion (FEIE)

The FEIE allows U.S. taxpayers living abroad to exclude a certain amount of their foreign-earned income from U.S. federal income tax.

For the tax year 2024, this exclusion amount is up to $126,500.

To qualify, you must pass either:

- Bona Fide Residency Test: You qualify if you are a resident of a foreign country for an uninterrupted period that includes an entire tax year.

- Physical Presence Test: You qualify if you are physically present in a foreign country for at least 330 full days during a 12-month period.

Foreign Tax Credit (FTC)

The FTC helps you avoid double taxation by allowing you to take a credit for foreign taxes paid on income that is also subject to U.S. federal tax.

This credit can reduce your U.S. tax liability significantly, especially if you reside in a country with high tax rates.

Foreign Housing Exclusion (FHE)

The FHE allows you to exclude certain housing expenses from your federal and state taxable income, including rent, utilities (excluding telephone), and other reasonable expenses related to housing abroad.

The amount you can exclude is limited to a base amount plus housing expenses exceeding 16% of the FEIE limit.

Filing Utah state taxes from abroad

When filing Utah state taxes from abroad, it's essential to determine your residency status and use the appropriate forms:

- Form TC-40: This is the primary form used for filing Utah individual income tax returns for full-year residents. You need to report all income, regardless of where it was earned.

- Form TC-40: This is the primary form used for filing Utah individual income tax returns for full-year residents. You need to report all income, regardless of where it was earned.

Deadlines

- Standard Deadline: April 15. The deadline for filing Utah state taxes aligns with the federal tax deadline. This is the due date for both filing your return and paying any taxes owed.

- Automatic Extension for Expats: June 15. If you are living outside the U.S. on April 15, you may receive an automatic two-month extension to file your return and pay any amount due without requesting an extension, extending the deadline to June 15. However, interest on any unpaid taxes will accrue from the original April 15 deadline.

- Additional Extension: October 15. You can request a further extension by filing Form 502E, Application for Extension of Time to File Personal Income Tax Return, typically extending the deadline to October 15. This extension is for filing your return only, not for paying any taxes owed. Interest on any unpaid taxes will continue to accrue from the original April 15 deadline.

- Payment Deadlines. Regardless of filing extensions, any taxes owed must be paid by April 15 to avoid interest and late payment penalties. If you file an extension, ensure that your payment is postmarked by the due date to avoid additional charges.

Consequences of non-compliance with Utah state tax laws

- Late Filing Penalty: If you fail to file your Utah state tax return by the due date, you will incur a late filing penalty. This penalty is 5% of the unpaid tax per month, up to a maximum of 25% of the total unpaid tax. Additionally, if the return is more than 60 days late, the minimum penalty will be either $135 or 100% of the unpaid tax, whichever is less.

- Late Payment Penalty: For any tax that is not paid by the due date, a late payment penalty will be assessed. This penalty is 0.5% of the unpaid tax per month, up to a maximum of 25% of the unpaid tax amount. This means that if you delay payment, you will continue to accumulate penalties each month until the tax is paid in full.

- Interest Charges: In addition to penalties, interest is charged on any unpaid taxes from the original due date until the taxes are paid in full. The interest rate is determined quarterly and, as of 2023, is 1.25% per month for both personal and business taxes. This interest continues to accrue until the full balance, including any penalties, is paid.

Audits and assessments

Utah may conduct residency audits to verify your residency status and ensure proper tax compliance. During an audit, you must provide extensive documentation, such as proof of domicile and detailed financial records. Failure to provide adequate documentation can result in additional tax assessments and penalties.